Breaking the Debt Cycle: A 90-Day Plan to Financial Freedom

- Shaksha

- Jun 30, 2025

- 6 min read

Updated: Jul 10, 2025

Have you ever found yourself stuck in a never-ending cycle of debt, where each payment feels like a drop in an ocean? It's easy to feel overwhelmed when bills keep piling up, and it seems like there's no way out. But the truth is, breaking free from the debt cycle is possible with the right approach and strategies. You don’t need a perfect past to start building a better financial future.

In this blog, we’ll walk you through a practical 90-day plan that will help you regain control of your finances, tackle your debt, and set you on the path to financial freedom. Whether you’re dealing with credit card debt, loans, or overdue bills, the right steps can make a significant difference. With consistent effort, commitment, and proven strategies, you can escape the debt trap and pave the way for a brighter financial future.

Why Breaking the Debt Cycle is Essential

Living in debt can feel like a constant burden. With high-interest rates, missed payments, and looming bills, it’s easy to feel trapped. The psychological and financial toll of debt can affect not only your finances but also your health, relationships, and overall well-being.

Breaking the cycle is critical for improving both your financial health and quality of life.

A well-organized, actionable plan to eliminate debt will help you reduce the stress of managing multiple bills and interest charges. As you start to make progress, you'll regain control and feel empowered to build a more secure financial future. Additionally, breaking the debt cycle also means improving your credit score, as timely payments and debt reduction contribute to better credit health.

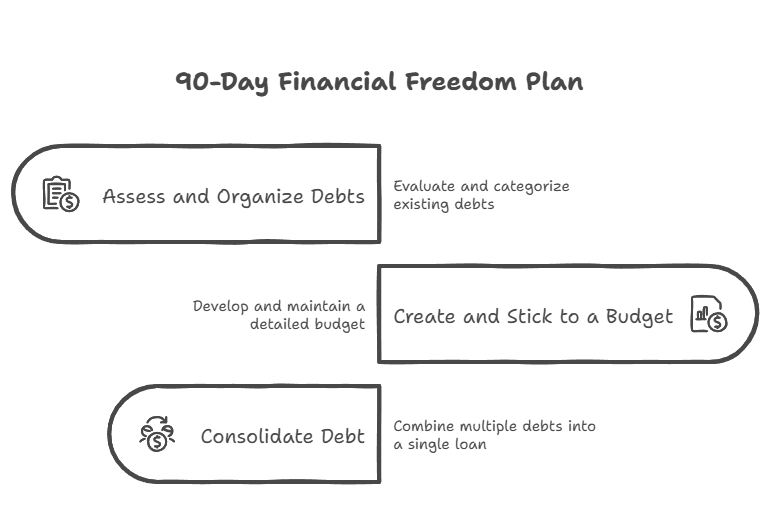

The 90-Day Plan to Financial Freedom

Breaking the cycle isn’t something that happens overnight, it requires dedication, time, and a clear strategy. This 90-day plan is divided into three key phases to help you pay down your debts, develop healthier financial habits, and build a solid foundation for long-term financial success.

Day 1-30: Assess and Organize Your Debts

The first step to breaking the cycle is understanding where you stand financially. Gather all your bills, loans, and credit statements, and create a comprehensive list of your debts. Write down the total amount owed, interest rates, and due dates for each account. While it may feel overwhelming, understanding the full extent of your debt is essential for creating an effective strategy.

Progress Milestone for Day 30:

List all debts with amounts, interest rates, and due dates.

Prioritize your debts using the “debt avalanche” or “debt snowball” method.

Once everything is organized, focus on prioritizing your debts. Start by paying off those with the highest interest rates first, such as credit card debt or payday loans, using the “debt avalanche” method. If you have smaller debts, you might want to consider using the “debt snowball” method, paying off small balances to gain momentum and motivation.

How Quicksettle Helps:

At Quicksettle, we can assist by negotiating with your creditors to reduce interest rates or create more favorable repayment plans. Our debt management experts work directly with your creditors to ensure your repayment plan is realistic and manageable.

Day 31-60: Create and Stick to a Budget

Now that you’ve organized your debts, it’s time to take control of your spending. A solid budget is crucial for breaking the cycle and ensuring that you stay on track with your debt repayment. Track your income and expenses for the next 30 days. Categorize your spending into needs, wants, and savings, and identify areas where you can cut back.

Progress Milestone for Day 60:

Identify areas where you can reduce spending.

Set a monthly spending limit and allocate funds to debt repayment.

Budgeting Tips:

Cut Unnecessary Spending: Look for areas where you can reduce expenses, such as dining out, entertainment, or subscriptions you no longer use. Redirect this money toward paying off your debt.

Set Realistic Goals: Create a monthly spending limit and stick to it. Allocate a specific amount toward debt repayment each month, and don’t deviate from your plan.

Automate Payments: Set up automatic payments for your bills and loans to avoid late fees and missed payments. This ensures you're staying on top of your obligations without the risk of forgetting.

How Quicksettle Helps:

Quicksettle helps you track your expenses and find opportunities for debt consolidation, allowing you to streamline your payments. We negotiate with your creditors to lower your monthly payments and make them more manageable.

Day 61-90: Consolidate Debt and Build Healthy Financial Habits

After the first 60 days of assessing your financial situation and creating a budget, it's time to take more aggressive action toward eliminating your debt. In this phase, consider consolidating your debt, which involves combining multiple loans or credit card balances into one payment with a lower interest rate. This simplifies your payments and often reduces the amount of interest you pay over time.

Progress Milestone for Day 90:

Consolidate your debt to simplify repayments.

Keep a close eye on your credit progress.

Debt Consolidation Tips:

Evaluate Your Options: Research debt consolidation loans or balance transfer credit cards to find the best option for your needs. Be sure to compare interest rates and fees before committing.

Debt Settlement Programs: If you're struggling with larger amounts of debt and can't afford to pay in full, debt settlement programs can help. Companies like Quicksettle work with creditors to negotiate a reduced amount, allowing you to settle your debt for less than the full balance.

How Quicksettle Helps:

Quicksettle provides access to expert debt settlement services and consolidation loans. Our team negotiates with creditors to reduce your overall debt and create a personalized repayment plan that works for you. This ensures you have the right support to break free from debt.

The Role of Quicksettle in Breaking the Debt Cycle

At Quicksettle, we understand how overwhelming it can be to deal with multiple creditors and high-interest rates. That’s why we offer tools and services that simplify debt management and provide expert guidance to help you break the cycle. Whether you need help consolidating debt, negotiating lower interest rates, or accessing debt settlement services, Quicksettle is here to support you every step of the way.

By leveraging Quicksettle’s services, you can streamline your debt repayment process and fast-track your journey toward financial freedom. Our team works directly with your creditors to negotiate reduced interest rates and more favorable payment terms. This makes it easier to manage your finances and focus on building a better future.

Conclusion

We hope this blog has helped you understand the steps involved in breaking this cycle and the strategies you can use to take control of your financial future. By following a structured 90-day plan, staying disciplined, and leveraging services like Quicksettle, you can break free from debt and achieve lasting financial freedom. Managing your debt wisely ensures a healthier financial future, helping you build a secure foundation for long-term success.

At Quicksettle, we’re here to guide you through the debt management process, ensuring that you don’t just break free from debt, but set yourself up for a better tomorrow. Start today and break the cycle!

Frequently Asked Questions (FAQs)

1. How long does it take to break the cycle?

Breaking the cycle depends on your income, debt amount, and commitment to the plan. With consistent effort, most people make significant progress within 90 days.

2. Can debt consolidation help me break the cycle?

Yes, debt consolidation can simplify payments and reduce interest rates, making it easier to pay off your debt faster.

3. Should I pay off all my debt at once?

It’s not always feasible to pay off all debt at once. Focus on paying off high-interest debt first, then gradually work on eliminating other debts.

4. How can I avoid falling back into debt?

After breaking the cycle, maintain a budget, save for emergencies, and avoid new debt. Financial discipline is crucial for maintaining freedom.

5. Is it possible to rebuild my credit while paying off debt?

Yes, timely payments and reducing your debt load will improve your credit score. Quicksettle’s tools help you manage debt and rebuild your credit effectively.

6. Can Quicksettle help me with debt consolidation?

Absolutely! Quicksettle offers debt consolidation, settlement, and management services to

help you regain control of your finances and fast-track the repayment process.

Comments